Your 3-item EOFY super checklist (and 3 changes to know for 1 July)

Hey friends,

The end of the financial year is looming!

Right now, in this small window before the financial year closes, a few moves are worth your attention.

This issue covers three actions to take before 30 June and three changes coming into effect on 1 July.

✅ Before 30 June: 3 things worth checking

1. Been salary sacrificing but haven’t hit the $30,000 cap? Top it up before 30 June.

If you’ve been salary sacrificing throughout the year but haven’t hit the $30,000 concessional cap, you can make a personal after-tax contribution to your super and claim it as a tax deduction.

The effect is the same as salary sacrifice. That gap gets taxed at 15% inside super instead of your marginal rate.

Check how much you’ve contributed this financial year through your super fund’s online portal.

Two things to keep in mind before you act.

If you’re paying via BPAY, allow at least a week for the funds to clear into your account before 30 June.

You’ll need to submit a Notice of Intent (NOI) to claim a deduction with your fund before lodging your tax return. Without it, the ATO won’t recognise the contribution as concessional.

2. Your 2020-21 carry-forward contributions are about to expire soon!

The carry-forward rule lets you draw on unused concessional cap from the previous five financial years, as long as your total super balance was under $500,000 on 1 July 2025.

The catch: after 30 June 2026, any unused space from 2020-21 expires permanently. It drops out of the five-year window and you can’t get it back.

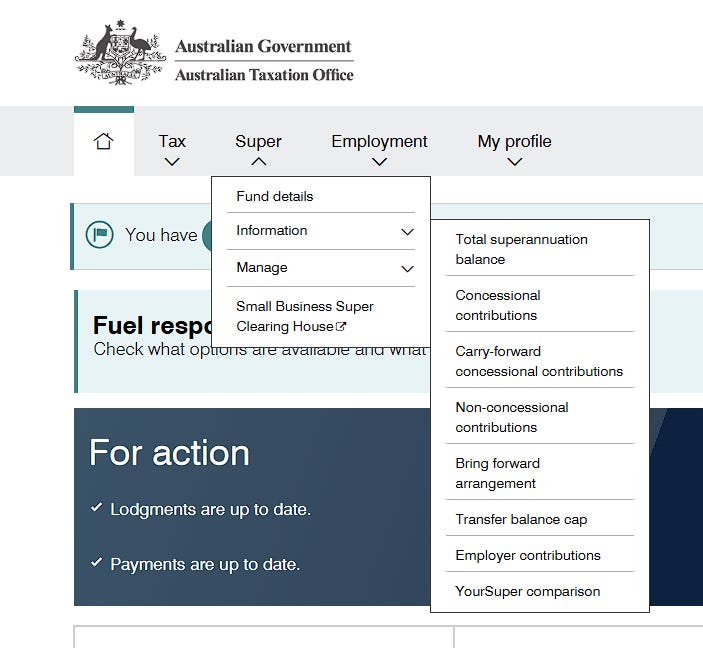

To check your balance, log into myGov and navigate to ATO online services, then “Super,” then “Information,” then “Carry-forward concessional contributions.” Takes about two minutes.

One note: in order to use your carry forward contributions, you must have already used up all of your concessional contributions this financial year. Which is currently $30,000.

3. Take advantage of the government super co-contribution

This one flies under the radar for a lot of people.

If your income is under $62,488 this financial year, the government will co-contribute 50 cents for every after-tax dollar you voluntarily put into super, up to a maximum of $500. To get the full $500, you need to contribute $1,000 and earn under $47,488. The benefit tapers to zero at $62,488.

The money lands in your super account automatically after you lodge your tax return. No application needed.

📆 From 1 July: 3 things changing for the new financial year

1. The concessional cap is rising to $32,500

From 1 July 2026, the concessional cap increases from $30,000 to $32,500. That’s an extra $2,500 into super at 15% tax instead of your marginal rate.

If you have a salary sacrifice arrangement, review the dollar amount now and update it before your first July pay run. Your payroll team will need the new figure.

I’m increasing my own salary sacrifice by roughly $208 per month to capture the full $32,500 in FY27.

2. The non-concessional cap is also rising

The annual non-concessional cap (after-tax contributions) is rising from $120,000 to $130,000.

More meaningfully for larger lump-sum contributions: the three-year bring-forward rule increases from $360,000 to $390,000.

If you’re sitting on cash outside super and considering a big contribution, it may be worth waiting until after 1 July. Contributing $130,000 then instead of $120,000 now gets you an extra $10,000 inside the tax-advantaged environment in a single move.

3. Payday super is here from 1 July

Currently, employers pay super quarterly. From 1 July, they must pay it every pay cycle, at the same time as wages.

Your super balance will grow faster because contributions hit sooner and compound immediately. It also reduces the risk of employers sitting on unpaid super, which has historically cost workers hundreds of millions of dollars each year.

If you run a business, your payroll system needs to be ready before 1 July. If you’re an employee, you should start seeing super deposits alongside each payslip from July onwards.

🎬 Recent Video

These are the four ETFs I would personally invest in if I started over today!

💳 Credit Card/Point Deals

HSBC Star Alliance Card - Earn up to 35,000 Infinity MileageLands Miles (EVA Air) & Gold Status when you spend $4,000 in the first 90 days. $0 first year, $499 aftwards.

Note - The above are not affiliate links.

💸 Investing/Finance Apps I Use

These are all the investing/finance apps that I use on a day-to-day basis.

Moomoo - Get 38 free fractional shares for new users

Sharesight - Save 4 months when you upgrade to an annual premium plan

YouTrip - Travel money card, get $10 for free when you deposit any amount.

ING - 5.75% p.a. high-interest savings account. Earn $125 when using code Jbn574

Independent Reserve - $30AUD BTC when you sign-up & make first trade

Simply Wall St - Get 40% off paid plans to help with your stock research

Note - Some of the finance apps above are affiliate links, and I will earn a commission; however, it comes at no additional cost to you and helps support me as a creator.